Are you planning to buy a car and want to understand how much extra you’ll pay over time? Knowing how to calculate interest on a car loan can save you money and help you make smarter decisions.

But the numbers can seem confusing at first. Don’t worry—this guide will break it down step-by-step, so you can easily figure out what your car loan will really cost. By the end, you’ll feel confident about your next move and avoid surprises on your monthly bill.

Let’s dive in and uncover the simple way to calculate your car interest.

Types Of Car Loan Interest

Understanding the types of interest on a car loan helps you choose the best deal. Different loans use different methods to calculate interest. This affects how much you pay over time. Knowing the type of interest can save money and stress.

Interest types mainly include simple interest, compound interest, and fixed or variable rates. Each works in a unique way. Let’s explore each type to make sense of car loan interest.

Simple Interest Explained

Simple interest is easy to understand and calculate. It is charged only on the original loan amount. The rate stays the same throughout the loan period. This means you pay interest on the principal only. Simple interest often results in lower total interest.

Compound Interest Basics

Compound interest adds interest on both the principal and the interest already charged. It grows faster than simple interest. This means you pay interest on interest. Compound interest can increase the total cost of your loan quickly.

Fixed Vs Variable Rates

Fixed rates stay the same for the entire loan term. Your monthly payments do not change. This offers stability and easy budgeting. Variable rates change over time. They go up or down with market trends. Variable rates can lower payments but add uncertainty.

Credit: www.youtube.com

Key Factors Affecting Interest

Interest on a car loan depends on several key factors. These factors decide how much extra you pay over the loan period. Understanding them helps you plan your budget better. Each factor changes the interest amount in different ways.

Loan Amount Impact

The loan amount is the total money you borrow for your car. A larger loan means more interest to pay. Lenders charge interest based on this amount. Smaller loans usually have lower total interest but might have higher rates.

Loan Term Influence

The loan term is how long you take to repay the loan. Longer terms lower your monthly payment but increase total interest. Shorter terms mean higher monthly payments but less interest overall. Choosing the right term affects your total cost.

Credit Score Role

Your credit score shows how well you manage debt. Higher scores get lower interest rates. Lower scores mean higher rates and more interest cost. Improving your credit score can save money on car loans.

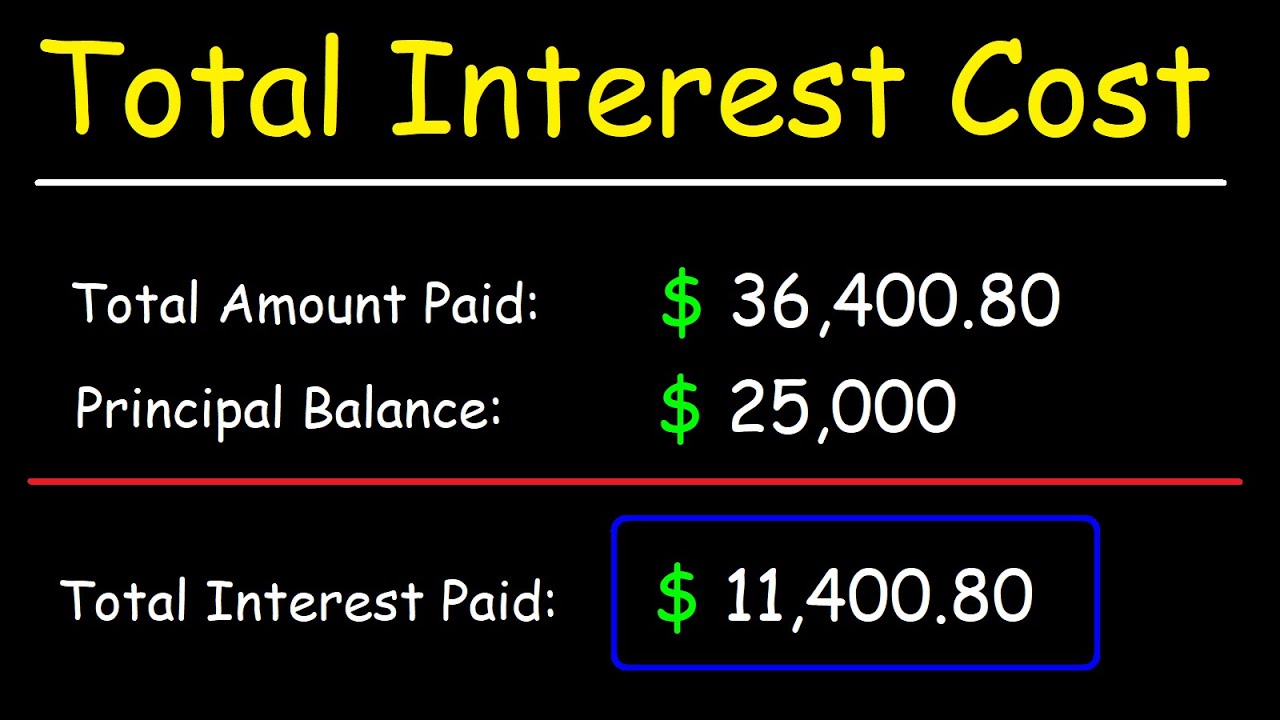

Step-by-step Interest Calculation

Calculating interest on a car loan helps you understand the total cost. It shows how much extra you pay over the loan’s life. Follow these clear steps to find out your interest amount.

Gathering Loan Details

Start by collecting key loan information. Find the loan amount, interest rate, and loan term. The loan amount is the money you borrow. The interest rate is the yearly cost of borrowing. The loan term is how many months or years you will pay.

Using The Simple Interest Formula

The simple interest formula is easy to use. Multiply the loan amount by the interest rate and loan term. Use this formula: Interest = Principal × Rate × Time. The principal is the loan amount. The rate is the annual interest rate in decimal form. The time is the loan term in years.

Calculating Monthly Payments

Divide the total interest by the number of months. Add this result to the loan amount. This gives the total amount to pay. Then, divide by the loan term in months. The result is your monthly payment. This method works for simple interest loans. For other loans, check with your lender.

Credit: www.exceltactics.com

Tools To Simplify Calculations

Calculating interest on a car loan can feel tricky. The math might seem complex at first. Thankfully, some tools make the process simple and clear. These tools help you see exactly how much interest you will pay over time. They save time and reduce mistakes. Using these tools gives you more control over your car loan decisions.

Online Calculators

Online calculators are easy to use and free. You just enter the loan amount, interest rate, and loan term. The calculator then shows the total interest and monthly payments. Many websites offer these calculators. They update instantly when you change numbers. These tools help you compare different loan offers quickly. No need for paper or a calculator.

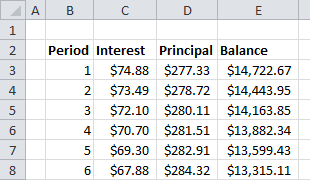

Spreadsheet Templates

Spreadsheet templates work well for detailed plans. You can download or create them in Excel or Google Sheets. They allow you to input loan details and see the interest broken down by month. Spreadsheets update automatically when you change data. You can save your work and track different loans. These templates provide a clear view of how payments affect your balance.

Tips To Reduce Interest Costs

Reducing interest costs on a car loan saves money over time. Small changes in your loan strategy can lower the total interest you pay. These tips help you manage your loan better and pay less in interest.

Improving Credit Score

A higher credit score usually means lower interest rates. Pay bills on time and reduce debt to boost your score. Check your credit report for mistakes and fix them quickly. Lenders see good credit scores as less risky. Better scores often lead to better loan offers.

Choosing Shorter Loan Terms

Shorter loans have higher monthly payments but lower interest costs. Interest builds up over time, so less time means less interest. Pick the shortest loan term you can afford. This reduces the total interest paid and helps you own your car faster.

Making Extra Payments

Extra payments reduce the loan balance faster. This lowers the interest calculated on your remaining balance. Even small extra payments make a big difference over time. Check with your lender to avoid prepayment penalties. Pay extra whenever possible to save on interest.

Common Mistakes To Avoid

Calculating interest on a car loan can be tricky. Many people make simple errors that increase the total cost. Avoiding these mistakes saves money and stress. Focus on the key factors that affect your loan interest.

Ignoring Additional Fees

Some buyers forget about extra fees in the loan. Fees like loan setup, processing, or late payment charges add up. These fees increase the total amount you pay over time. Always ask for a full list of fees before signing any documents. Add these fees to your interest calculations for a true cost.

Misunderstanding Rate Types

Loan rates come in different types. Fixed rates stay the same during the loan term. Variable rates can change with the market. Confusing these can lead to surprise payments. Check your loan agreement carefully. Know if your rate changes and when it happens. This knowledge helps you plan your budget better.

Credit: www.wikihow.com

Frequently Asked Questions

How Do You Calculate Simple Interest On A Car Loan?

Simple interest is calculated by multiplying the principal loan amount, interest rate, and loan term. The formula is Interest = Principal × Rate × Time. This method is straightforward and gives you the total interest over the loan period.

What Factors Affect Car Loan Interest Calculation?

The main factors include the loan amount, interest rate, loan term, and payment frequency. Credit score and lender policies also impact the rate. These elements determine how much interest you pay overall.

How Does Compound Interest Work On Car Loans?

Compound interest means interest is calculated on the initial amount plus accumulated interest. This increases the total interest paid compared to simple interest. It’s less common in car loans but important to understand.

Can I Calculate Interest On A Car Loan Monthly?

Yes, most car loans calculate interest monthly based on the outstanding balance. Monthly calculations help in understanding how payments reduce principal and interest over time.

Conclusion

Calculating interest on a car loan helps you plan your budget. Knowing the rate and loan term makes payments clear. Use simple formulas or online calculators to find costs. This knowledge saves money and avoids surprises later. Always check the total interest before signing any deal.

Understanding interest keeps your finances healthy and stress-free. Keep these tips in mind for smart car buying.

As an Amazon Associate, I earn from qualifying purchases.