Are you wondering if refinancing your home is a smart move? It’s a big decision that can save you money or cause unexpected costs.

Imagine lowering your monthly payments or paying off your mortgage faster—sounds great, right? But there’s more to consider before you take the plunge. You’ll discover the key factors that can help you decide if refinancing is right for you. Keep reading to find out how to make the best choice for your financial future.

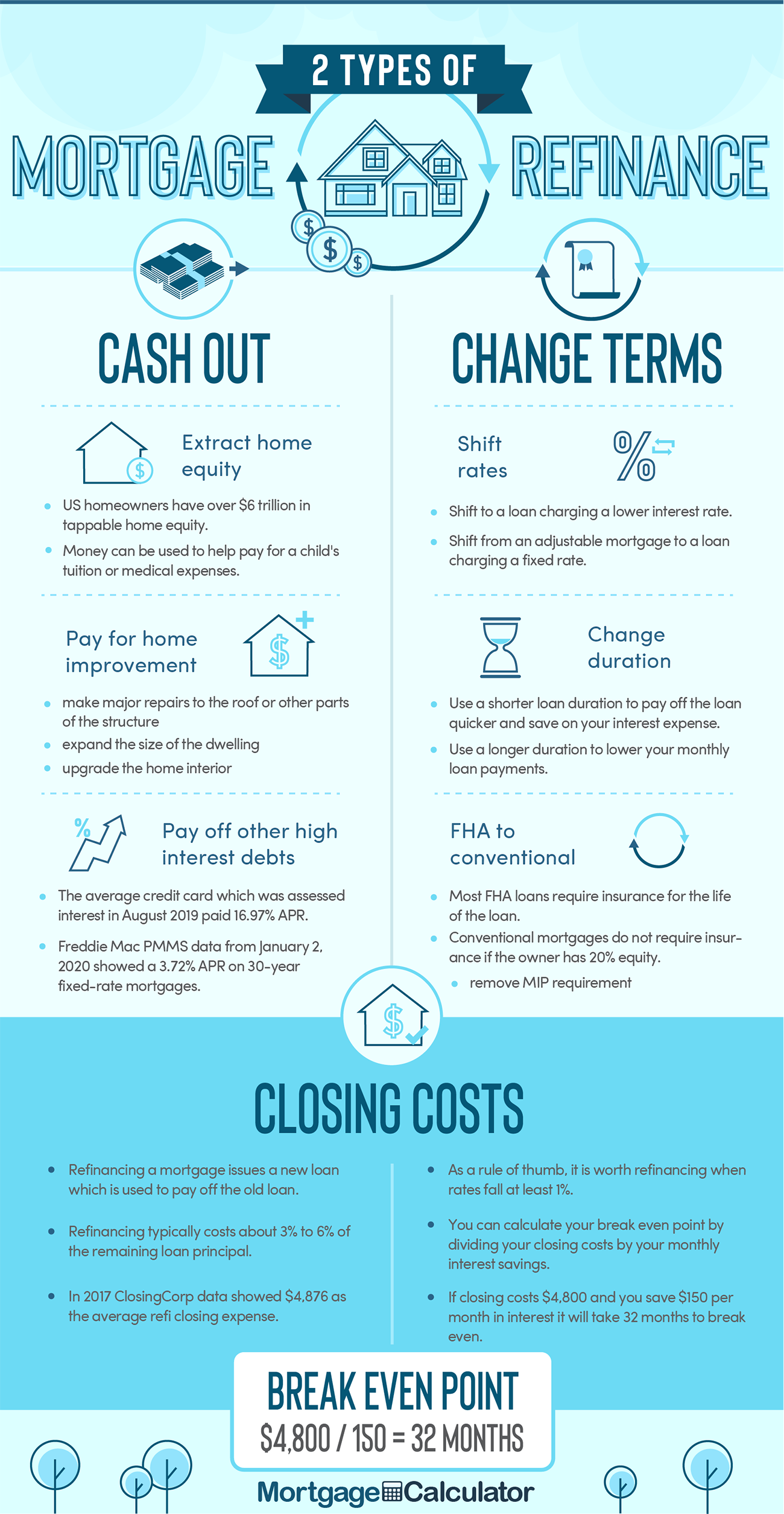

When To Consider Refinancing

Refinancing your home can save money or change your loan to fit your needs better. It is smart to refinance at the right time. Knowing when to consider refinancing helps you make the best choice for your finances.

Interest Rate Drops

Interest rates often change. If rates fall below your current rate, refinancing may lower your monthly payments. Even a small drop can save you money over time. Watch for rate changes from banks and lenders.

Changing Loan Terms

Refinancing lets you change your loan length or type. You can switch from an adjustable-rate to a fixed-rate loan. Shortening your loan term may increase payments but reduces total interest. Extending your term lowers monthly payments but costs more in interest.

Improving Credit Score

A better credit score may get you lower interest rates. Refinancing after your credit improves can save money. Check your credit before refinancing to see if rates will be better. A higher score means lenders trust you more.

Life Changes Impacting Finances

Big life changes affect your money needs. A new job, marriage, or more family members can change your budget. Refinancing can adjust your loan to fit new expenses. Use refinancing to ease financial stress during life changes.

Benefits Of Lower Interest Rates

Lower interest rates offer clear benefits for homeowners considering refinancing. They can make your mortgage more affordable and reduce the total cost over time. Understanding these benefits helps you decide if refinancing fits your financial goals.

Reducing Monthly Payments

Lower interest rates mean smaller monthly mortgage payments. This frees up cash for other expenses or savings. A lower payment can ease financial pressure and improve your budget. Many homeowners find extra money for bills, groceries, or emergencies.

Saving On Interest Over Time

Paying less interest saves a lot during your loan term. Even a small rate drop can cut thousands from total interest costs. This means more of your payment goes to the loan balance. Over years, savings add up, helping you build home equity faster.

Switching Loan Types

Switching loan types during refinancing can change your monthly payments and loan terms. Choosing the right loan type depends on your financial goals and risk tolerance. Understanding the difference between fixed and adjustable rates helps you make a smart choice. Here’s a look at what switching involves.

Fixed To Adjustable Rates

Switching from a fixed to an adjustable rate might lower your initial monthly payment. Adjustable rates start low but can change after a set period. This change depends on market interest rates. You might save money early on, but payments can rise later. This option suits those who plan to sell or refinance soon.

Adjustable rates offer flexibility but carry risk. Your payment could increase, making budgeting harder. Consider how long you will stay in the home before choosing this option. A shorter stay might make adjustable rates more attractive.

Adjustable To Fixed Rates

Switching from adjustable to fixed rates gives payment stability. Your monthly payment stays the same over the loan term. This helps with budgeting and reduces surprise increases. Fixed rates usually start higher than adjustable rates but protect against rising interest costs.

This switch suits homeowners who want financial security. It is useful if rates are low and expected to rise. Fixed rates provide peace of mind with steady payments. Think about your long-term plans before refinancing this way.

Accessing Home Equity

Accessing home equity is a common reason many homeowners consider refinancing. Home equity is the part of your home you truly own. It grows as you pay off your mortgage or when your home value rises. Refinancing can let you use this equity for different needs.

Using home equity through refinancing can provide cash for big expenses. It offers an option to borrow money at lower rates than other loans. This makes it easier to manage large costs without high interest.

Cash-out Refinancing

Cash-out refinancing means taking a new loan for more than your current mortgage. The extra amount comes to you as cash. You can use this money for repairs, debt, or other needs.

This method replaces your old loan with a new one. It often has a lower interest rate. It helps to get funds without applying for separate loans.

Funding Major Expenses

Many people use home equity to pay for big costs. Home improvements, college fees, or medical bills are common examples. Using equity can save interest compared to credit cards or personal loans.

This approach spreads out payments over time. It avoids high monthly bills. Careful planning is key to avoid financial stress later.

Improving Loan Terms

Refinancing your home can improve your loan terms in ways that save money and reduce stress. Changing your loan details might lower monthly payments or cut the total interest paid. Refinancing also gives you control over how long you want to stay in debt.

Shortening Loan Duration

Refinancing to a shorter loan period means paying off your home faster. This change reduces the amount of interest you pay over time. Your monthly payment may rise, but the total cost of the loan drops. Shorter loans help you build equity quicker and free you from debt earlier.

Removing Private Mortgage Insurance

Private Mortgage Insurance (PMI) adds extra cost to many home loans. Refinancing can remove PMI if your home’s value has grown or you have paid down enough principal. Dropping PMI lowers your monthly bill and saves money every month. This step makes your mortgage more affordable and clearer.

Credit: www.mortgagecalculator.org

Costs And Risks Of Refinancing

Refinancing your home can save money on interest or lower monthly payments. Yet, it also has costs and risks that need careful thought. Knowing these helps you decide if refinancing is right for you.

Closing Costs And Fees

Refinancing comes with closing costs. These include appraisal fees, application fees, and title insurance. These fees can add up to 2% to 5% of the loan amount. Paying these costs upfront or adding them to the loan can affect your savings.

Impact On Credit Score

Applying for refinancing means a credit check. This can lower your credit score slightly. Multiple credit checks in a short time can lower it more. A lower credit score might increase future loan costs.

Longer Loan Terms

Refinancing often means starting a new loan term. This can extend your repayment period. A longer loan term may lower monthly payments but increase total interest paid. Think about how long you plan to stay in the home.

Steps To Refinance Successfully

Refinancing your home can save money and reduce monthly payments. Success depends on careful planning. Follow clear steps to make the process smooth and beneficial.

Evaluating Your Financial Situation

Check your credit score and debt levels first. Know your current interest rate and loan balance. Calculate how much you can afford to pay monthly. Understand your financial goals for refinancing.

Comparing Lenders And Offers

Look at different lenders for the best rates. Compare loan terms and fees carefully. Note any special offers or discounts. Choose the lender that fits your needs best.

Gathering Necessary Documentation

Collect pay stubs, tax returns, and bank statements. Prepare your current mortgage documents and ID. Organize these papers for easy access. This speeds up the refinancing process.

Preparing For The Application Process

Fill out the loan application accurately. Answer all lender questions honestly and clearly. Stay ready for credit checks and appraisals. Keep communication open with your lender for updates.

Credit: www.banklandmark.com

Credit: mmccu.com

Frequently Asked Questions

What Are The Benefits Of Refinancing Your Home Loan?

Refinancing can lower your interest rate, reduce monthly payments, or shorten your loan term. It may also allow access to home equity for other expenses, providing financial flexibility and potential savings over time.

When Is The Best Time To Refinance A Mortgage?

The best time is when interest rates drop significantly below your current rate. Also, consider refinancing if your credit score has improved or your financial situation has changed positively.

How Does Refinancing Affect My Credit Score?

Refinancing may cause a small, temporary dip in your credit score due to a hard inquiry. However, timely payments on the new loan can improve your credit over time.

Are There Risks Involved In Refinancing A Home?

Yes, risks include closing costs, longer loan terms increasing total interest paid, and potential loss of benefits from your original mortgage. Evaluate carefully before deciding to refinance.

Conclusion

Refinancing your home can save you money on interest. It might lower your monthly payments or shorten your loan term. Think about your current loan and future plans first. Costs like fees and closing expenses also matter. Weigh the savings against these costs carefully.

Talk to a trusted lender to get clear answers. Making a smart choice depends on your personal situation. Consider all factors before deciding to refinance your home.

As an Amazon Associate, I earn from qualifying purchases.